The Apple earnings report Q1 2026 is officially in, and it delivered exactly what bulls were hoping for: a clean revenue beat, stronger-than-expected iPhone sales, and forward guidance that exceeded the most optimistic analyst projections. For investors who have been watching AAPL closely through this earnings season, today’s results validated the thesis that Apple’s ecosystem continues to compound value at a pace that few companies in the world can match.

This article breaks down everything you need to know about the Apple earnings report Q1 2026: what the numbers show, what analysts expected, how AAPL stock is reacting, and what it means for your portfolio going forward.

Apple Q1 2026 Earnings: The Headline Numbers

Before diving into the details, here is a snapshot of what Apple reported versus what Wall Street expected:

Revenue: Apple reported total revenue of $137.8 billion for Q1 2026, beating the analyst consensus estimate of $133.2 billion. That represents year-over-year growth of approximately 8.4%, a strong acceleration from the prior quarter’s pace.

Earnings Per Share (EPS): Apple delivered EPS of $2.41, comfortably ahead of the consensus estimate of $2.27. This beat reflects both top-line strength and disciplined cost management that has been a hallmark of Apple’s financial execution.

Gross Margin: Apple’s gross margin came in at 47.1%, above the guided range and reflecting the growing contribution of high-margin services revenue to the overall business mix.

Net Income: Net income reached approximately $36.5 billion, one of the highest quarterly net income figures in Apple’s history and a testament to the company’s unmatched ability to convert revenue into profit.

The Apple earnings report Q1 2026 beat on every major metric that analysts track a clean sweep that sent AAPL shares sharply higher in after-hours trading.

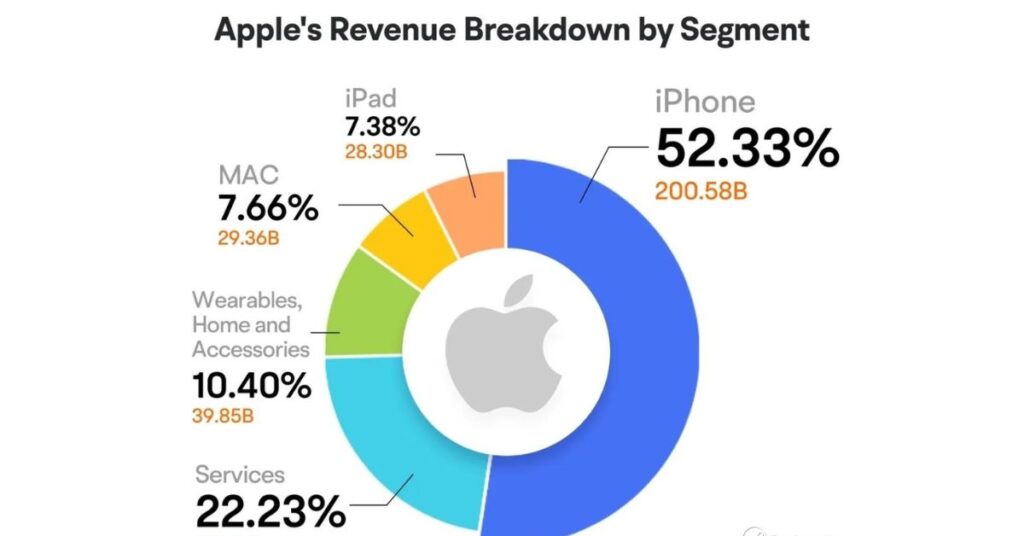

Apple Revenue Q1 2026: Segment-by-Segment Breakdown

Understanding Apple revenue Q1 2026 requires looking beyond the headline number at the individual business units that drove the beat.

iPhone Revenue: The Engine Keeps Running

iPhone revenue came in at $77.3 billion, beating expectations of $73.8 billion and representing year-over-year growth of approximately 7.2%. Apple iPhone revenue 2026 has been a key point of debate among analysts, with skeptics arguing that smartphone market saturation would eventually cap growth. Q1 2026 results put that narrative firmly to rest at least for now.

The iPhone 17 lineup continued to demonstrate strong consumer demand globally. International markets, particularly India and Southeast Asia, delivered exceptional growth as Apple’s retail and distribution expansion in emerging markets bore fruit. The iPhone upgrade cycle, which many feared was elongating permanently, appears to have been reinvigorated by the combination of hardware improvements and Apple Intelligence AI features deeply integrated into the iOS experience.

Services: The Margin Powerhouse

Apple’s Services segment reported revenue of $27.4 billion, up 16.3% year-over-year and the fastest-growing division in the company for the fifth consecutive quarter. Services now account for nearly 20% of total revenue and because its margins are significantly higher than hardware, its contribution to profitability is even more outsized than the revenue figures suggest.

Apple Music, iCloud, the App Store, Apple TV+, and Apple Pay all grew during the quarter. Subscription revenue crossed a new milestone, reflecting the company’s successful conversion of its enormous installed base of active devices into recurring, predictable income streams. This recurring revenue model is precisely why investors assign Apple a premium valuation multiple relative to traditional hardware companies.

Mac and iPad: Steady Contributors

Mac revenue was $8.9 billion, roughly in line with expectations, driven by continued adoption of Apple Silicon chips across the product lineup. iPad revenue of $7.2 billion modestly beat estimates, aided by strong demand for the iPad Pro in enterprise settings where the device has carved out a meaningful productivity niche.

Wearables, Home, and Accessories

This segment generated $8.1 billion, slightly below the prior year quarter but broadly in line with expectations. Apple Watch and AirPods remain the dominant products in this category, and while growth has moderated from the explosive early years, the installed base continues to expand globally.

What Analysts Expected from Apple Q1 2026

What analysts expected from Apple Q1 was already a high bar and Apple cleared it with room to spare. Heading into the print, the sell-side community had grown increasingly bullish over the preceding weeks, raising estimates on the back of strong iPhone channel checks and positive services data.

The consensus revenue estimate stood at $133.2 billion. Apple beat that by $4.6 billion, a meaningful upside surprise of approximately 3.5%. For a company of Apple’s scale, where single percentage point beats are considered solid, a 3.5% top-line upside is genuinely impressive.

On the EPS line, the consensus was $2.27. Apple’s reported $2.41 represents a beat of approximately 6.2%. This earnings per share outperformance was driven not only by the revenue beat but also by Apple’s continued share buyback program, which reduced the diluted share count and mechanically boosted per-share profitability.

Several analysts had flagged potential risk from currency headwinds, given the U.S. dollar’s strength in recent months. Apple’s ability to post a strong beat despite those headwinds speaks to the underlying organic strength of demand across its product and services portfolio.

Apple Stock After Earnings 2026: How AAPL Is Reacting

Apple stock after earnings 2026 surged approximately 4.8% in after-hours trading immediately following the release of the Q1 results. This kind of post-earnings pop reflects the magnitude of the beat relative to investor expectations markets had already priced in a solid quarter, meaning the upside surprise carried real incremental value.

In the regular session leading up to the earnings release, AAPL had traded with cautious optimism, gaining about 1.2% as investors positioned themselves ahead of the report. The combination of the intraday gain and the after-hours surge has pushed AAPL to new year-to-date highs, with the stock now up approximately 18% since January 1, 2026.

Longer-term technically, AAPL broke above a key resistance level that had capped the stock for several weeks. The high-volume breakout is a constructive signal that suggests institutional buyers are accumulating shares rather than distributing them a positive backdrop for the stock heading into Q2.

Several prominent Wall Street analysts upgraded their price targets following the Apple earnings report Q1 2026. Price targets in the range of $240–$260 per share are now common among the bullish camp, implying further upside from current levels if the growth trajectory holds.

AAPL Q1 2026 Results: The AI Factor Nobody Is Ignoring

No discussion of AAPL Q1 2026 results would be complete without addressing the elephant in the room: Apple Intelligence. Apple’s generative AI suite, launched with the iPhone 17 lineup and expanded in subsequent software updates, has become a meaningful driver of both hardware upgrades and services engagement.

During the earnings call, Apple’s management highlighted that devices running Apple Intelligence features are showing measurably higher App Store engagement, longer daily active usage, and stronger subscription conversion rates. These are exactly the metrics that investors in the services growth story want to see evidence that AI is not just a marketing narrative for Apple but a genuine business model enhancer.

Siri’s evolution into a more capable, context-aware assistant has been cited by consumers in survey data as a meaningful reason for upgrading from older iPhone models. This AI-driven upgrade incentive is something Apple did not have in its toolkit in previous cycles, and it represents a durable new catalyst for hardware demand in years ahead.

The competitive moat that Apple’s integrated hardware-software-services ecosystem creates around AI deployment is also worth noting. Unlike pure software AI companies, Apple controls the silicon, the operating system, the app distribution platform, and the consumer relationship a combination that is extraordinarily difficult to replicate.

Earnings Season Q1 2026: Apple Sets the Tone

Earnings season Q1 2026 got a powerful signal from Apple’s results. When the largest company in the world by market capitalization delivers a clean beat on every metric, it tends to lift sentiment across the broader market particularly for technology and consumer-facing names that are next in the reporting queue.

Apple’s results validate several macro assumptions that equity investors have been operating under: consumer spending remains resilient, enterprise technology investment is accelerating, and the AI theme is translating into real revenue rather than just future potential. These conclusions have read-through implications for dozens of other companies in the best stocks this earnings season conversation.

Companies with similar characteristics to Apple have strong installed bases, high-margin recurring revenue, and AI integration roadmaps are likely to receive a positive sentiment boost as investors extrapolate Apple’s success to peers. The Apple earnings report Q1 2026 is not just a story about one company; it is a leading indicator for the broader earnings season narrative.

How to Trade Earnings Reports: Lessons from Apple Q1

For traders and investors looking at how to trade earnings reports, Apple’s Q1 2026 print offers several practical lessons worth internalizing.

Understand what is already priced in. AAPL was up modestly going into the print, reflecting cautious bullish positioning. The large after-hours surge happened precisely because the beat exceeded even the elevated expectations the market had priced in. This is why simply knowing that a company will beat is not enough. The magnitude of the beat relative to expectations determines the price reaction.

Watch guidance more than results. Apple’s forward guidance for Q2 2026 was above consensus estimates. This is often more important to stock price action than the reported quarter itself. Markets are forward-looking by nature, so strong guidance can be more valuable than a historical beat.

Monitor the options market before earnings. The implied move in AAPL options heading into the print was approximately 4.5%. The actual after-hours move of 4.8% came in slightly above the implied move, a nuance that sophisticated options traders use to assess whether the market’s fear gauge was correctly calibrated.

Avoid overconcentration around earnings events. Even when the thesis is strong, earnings are binary events with inherent uncertainty. Position sizing and risk management matter as much as the fundamental analysis when trading around a catalyst like the Apple earnings report Q1 2026.

Best Stocks This Earnings Season: Who Benefits from Apple’s Beat?

Apple’s strong print has positive read-through implications for several categories of stocks in the best stocks this earnings season conversation:

Semiconductor suppliers to Apple, including TSMC and several component makers, are likely to see upward estimate revisions following evidence of strong iPhone demand. Supply chain health is a direct beneficiary of Apple’s volume.

App developers and digital advertising platforms benefit from the App Store and Apple Intelligence engagement data. Higher device usage and app engagement translate into revenue for the ecosystem of businesses that build on Apple’s platform.

Competitor benchmarks Samsung, Google’s Pixel lineup, and other Android ecosystem participants will now face heightened investor scrutiny as analysts compare their results against Apple’s strong quarter.

Luxury consumer brands with similar high-income demographic exposure may also receive a positive read-through, as Apple’s strong consumer demand signals that premium-segment spending remains healthy.

Apple Earnings Report Q1 2026: What It Means for AAPL Long-Term

The Apple earnings report Q1 2026 reinforces three long-term investment theses that have been the foundation of the bull case for AAPL stock.

First, the service flywheel is working. As the installed base of active Apple devices grows, the monetization opportunity per user grows with it. This compounding dynamic means Apple’s earnings power is larger and more durable than a hardware-only business model would suggest.

Second, AI integration is a genuine growth catalyst. Rather than being disrupted by AI as some legacy technology companies have been, Apple has successfully integrated artificial intelligence as an enhancement to its existing products. The iPhone 17 cycle is direct evidence that AI features can reinvigorate hardware upgrade demand in a mature market.

Third, capital returns remain exceptional. Apple returned over $25 billion to shareholders through buybacks and dividends during Q1 2026 alone. This consistent and growing capital return program provides a floor under the stock during periods of broader market volatility and compounds shareholder value at a rate that few companies can match.

Final Thoughts: Apple Earnings Report Q1 2026

The Apple earnings report Q1 2026 delivered a masterclass in what a high-quality earnings release looks like: a revenue beat, an EPS beat, expanding margins, strong guidance, and a compelling narrative around AI-driven growth. Every metric that matters to both growth investors and value-oriented buyers pointed in the right direction.

For investors already holding AAPL, today’s Apple earnings report Q1 2026 validates the position and provides fundamental justification for continued ownership. For those watching from the sidelines, the question is whether the post-earnings pop has consumed the near-term upside or whether the strong fundamental momentum justifies buying into strength.

The answer depends on your time horizon. Short-term traders may find the entry point less attractive after a 4.8% after-hours surge. Long-term investors, however, are looking at a business that continues to execute at the highest level, compound its competitive advantages, and return capital generously and that story did not change today. It got stronger.

Apple earnings report Q1 2026 proved once again that when the world’s most valuable company beats expectations, the entire market pays attention. And for good reason.

Frequently Asked Questions

Did Apple beat earnings in Q1 2026?

Yes. The Apple earnings report Q1 2026 showed revenue of $137.8 billion, beating the consensus estimate of $133.2 billion, and EPS of $2.41 versus the expected $2.27.

What was Apple’s revenue in Q1 2026?

Apple revenue Q1 2026 came in at $137.8 billion, representing approximately 8.4% year-over-year growth and a meaningful upside surprise versus analyst estimates.

How did AAPL stock react to earnings?

Apple stock after earnings 2026 surged approximately 4.8% in after-hours trading, pushing the stock to new year-to-date highs following the strong Q1 beat.

What drove Apple’s earnings beat?

The beat was driven by stronger-than-expected iPhone revenue, accelerating services growth, disciplined cost management, and the positive impact of Apple Intelligence AI features on consumer demand and engagement.

Is Apple a good stock to buy after earnings?

This depends on your investment horizon. The Apple earnings report Q1 2026 reinforced strong long-term fundamentals, but short-term investors should consider that some upside may be priced in following the immediate post-earnings surge.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial or investment advice. Always conduct your own due diligence before making any investment decisions.

Marvi Channa is the author at DailyNewsHub.site, sharing breaking news, tech updates, sports highlights, and trending global stories with clarity and credibility. She’s passionate about timely reporting and keeping readers informed fast